Montreal’s real estate market outperformed other major cities in Canada, despite relatively flat summer activity

Royal LePage® maintains its year-end forecast in anticipation of further interest rate cuts by the Bank of Canada, which will be felt more acutely in early 2025

Third-quarter highlights:

- The aggregate price of a home in Greater Montreal rose above $600,000 in the third quarter of 2024, up 1.0% compared with the previous quarter.

- The Greater Montreal Area market is faring well, with a slight quarterly increase in property prices, while the greater Toronto and Vancouver markets posted declines.

- The aggregate price of a home in the region is expected to increase by 1.6% between the third and fourth quarters.

- Royal LePage applauds Ottawa’s move to improve access to home ownership for Canadian first-time buyers by extending the mortgage amortization period by five years, although this will come at a price to borrowers.

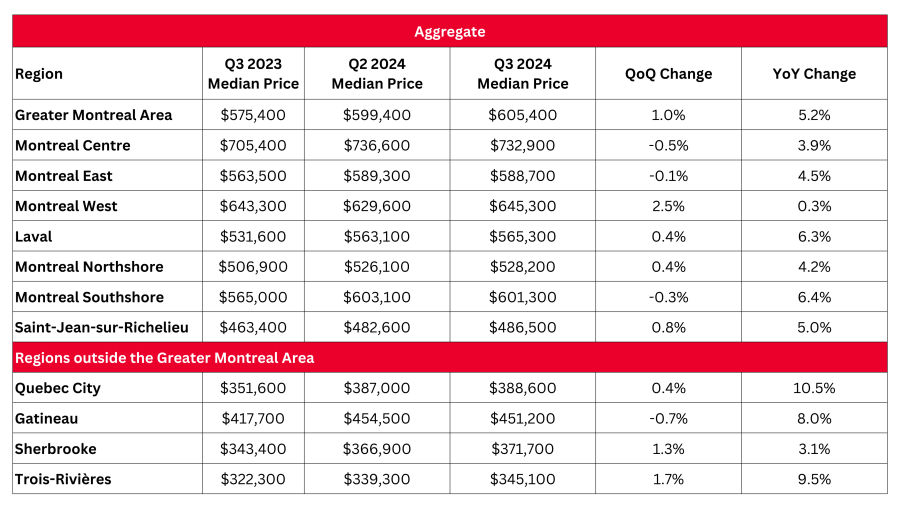

MONTREAL, Quebec, October 10, 2024 – Prices for residential properties in the Greater Montreal Area real estate market have risen slightly, according to the results of the Royal LePage House Price Survey and Market Forecast released today. During the third quarter of 2024, the aggregate[1] price of a home in the area was up by 5.2% compared to the same quarter in 2023, to $605,400, representing an increase of 1.0% on a quarterly basis.

MONTREAL, Quebec, October 10, 2024 – Prices for residential properties in the Greater Montreal Area real estate market have risen slightly, according to the results of the Royal LePage House Price Survey and Market Forecast released today. During the third quarter of 2024, the aggregate[1] price of a home in the area was up by 5.2% compared to the same quarter in 2023, to $605,400, representing an increase of 1.0% on a quarterly basis.

When broken out by property type, the median price of a single-family detached home rose by 7.1% in the third quarter of 2024 compared to the same period in 2023, to $691,500, an increase of 1.5% on a quarterly basis. For condominiums, the median price saw a more modest increase last quarter, rising 4.0% year over year and 0.4% quarter over quarter, to $467,700. Price data, which includes both resale and new build, are provided by RPS Real Property Solutions, a leading Canadian real estate valuation company.

Though the Bank of Canada’s key lending rate has seen three consecutive reductions of 25 basis points each since June, down to 4.25%, and inflation fell to the central bank’s 2% target in August,[2] the long-awaited upswing in the Montreal property market failed to materialize. There are several reasons for this: the summer market reverted to seasonal norms where activity tends to be slower, and vacation activities took priority over house hunting for buyers who continued to monitor rumours of further rate cuts. Elsewhere in the country, the Greater Toronto Area and Greater Vancouver markets experienced slight corrections during the third quarter in response to a surge in supply, caused in part by investors putting units up for sale.

“Despite three Bank of Canada rate cuts, we have yet to see a buyer rush. On the one hand, buyers are standing by, confident that further rate cuts are imminent and will create a more opportune time to buy. On the other hand, sellers are fine-tuning their strategies, counting on a wave of motivated buyers in the next few months,” said Dominic St-Pierre, executive vice president, business development, Royal LePage. “The Greater Montreal Area real estate market is performing well, with healthy growth in activity and prices, considering that Canada’s other two major markets are stagnating.”

With another announcement by the Bank of Canada due on October 23rd, additional pent-up demand is expected to be released into the market. According to the latest predictions by economists, October will bring the fourth and penultimate drop in the key lending rate for 2024.

“The dilemma that seems to be keeping buyers awake at night is whether to jump in now before prices go up due to higher demand, or keep waiting and take advantage of even more attractive mortgage rates,” St-Pierre added. “We’re already seeing an uptick in activity, which began in September.”

The issue of supply remains

Although home supply has improved over the past year in Montreal, the number of housing starts remains below the historical average and is too low to keep up with demand from a growing population, according to the latest report from Canada Mortgage and Housing Corporation (CMHC).[3] Moreover, three out of every four units started in Montreal’s metropolitan area since January were rental apartments, according to CMHC, which means that resale market supply has not grown at the same pace.

30-year amortization period: a necessary measure that comes at a cost

In August and September, the Government of Canada announced significant adjustments aimed at improving affordability for first-time homebuyers. As of December 15th, lenders will be allowed to offer 30-year amortization periods on insured mortgages – where borrowers have a down payment of less than 20% – to first-time homebuyers and all buyers of new-build homes. Although this means borrowers will pay more interest over the life of the loan, it is a welcome advantage for future generations of buyers, allowing them to spread out their mortgage payments over an additional five years.

“We applaud the recent measures announced by the federal government,” said St-Pierre. “The housing affordability issue is a top priority for many, and we owe it to ourselves as a society to provide solutions for future generations who will be faced with the realities of a higher cost of living. That said, these new measures raise the age-old question: what impact will they have on real estate demand in terms of rising property prices in Canada in the context of a chronic housing shortage? In the short term, these measures are likely to fuel existing demand and drive up prices. However, in the long term, this easing of mortgage rules will help many first-time buyers access home ownership and build wealth.

“This financial leverage is not free. The longer the mortgage repayment timeline, the greater the interest burden for borrowers. As supply remains anemic relative to property demand, due to growing population, it is crucial that our governments continue to invest in short-, medium- and long-term solutions that will bring more homes onto the resale market.”

According to a recent survey conducted for Royal LePage by Hill & Knowlton,[4] nearly three-quarters of Canadians belonging to the adult generation Z and young millennial cohort – those aged 18 to 38, or born between 1986 and 2006 – say that home ownership is a priority for them. Just 54%, however, believe they can achieve that goal in their lifetime.

What to expect in the Greater Montreal Area market between now and year-end

After three years, the Bank of Canada succeeded in shepherding national inflation back to its target rate in August, to 2.0%. Inflation in Quebec cooled to 1.5% during the same month. At the same time, unemployment has continued to rise and households continue to face affordability challenges, while an increasing number of current homeowners are renewing their mortgages at higher rates. Meanwhile, consumer confidence is on the upswing. According to the latest report from the Conference Board of Canada, the consumer confidence in Canada index rose by 3.3% in September over the previous month, reaching its highest level in over a year.[5] As a result, the percentage of Canadians who feel that now is a good time to make a major purchase has increased.

“In light of this economic data, we remain confident that the Bank of Canada will reduce its key rate further by the end of 2024, but it remains to be seen by how much. Consequently, we expect buyers, especially first-time buyers, to be back in larger numbers during the first half of 2025. Our 2024 year-end forecast remains unchanged,” St-Pierre concluded.

As reported in its Q1 2024 House Price Survey, Royal LePage forecasts that the aggregate price of a property in the Greater Montreal Area will appreciate by 8.5% in the fourth quarter of 2024 compared to the same period in 2023, to $614,978, representing an increase of 1.6% from the third to the fourth quarter.

Provincial summary

In the third quarter of 2024, Quebec’s residential real estate markets showed divergent trends.

In Sherbrooke and Quebec City, the typically quieter summer market gained momentum, then showed the first signs of a slowdown at the end of September. In the Greater Montreal Area, the third quarter saw a return to seasonal norms, with transaction activity picking up in September. The majority of the province’s markets saw slight quarterly price increases, with aggregate values remaining higher than a year earlier in all reported regions.

Last quarter, the Quebec City market saw the largest year-over-year increase in aggregate prices among all Canadian regions in the report, rising 10.5% to $388,600. Over the same period, the aggregate price of a home in Gatineau, Sherbrooke and Trois-Rivières appreciated by 8.0%, 9.6% and 9.7%, respectively, year over year. In the Greater Montreal Area, the aggregate price of a home saw a sustained year-over-year increase of 5.2%, surpassing the $600,000 mark.

The Bank of Canada’s expected interest rate cut, or possibly cuts, in the fourth quarter will likely stimulate demand this autumn, leading to an early spring market. At the same time, the extension of the 30-year mortgage amortization period for first-time buyers may encourage those who had been priced out of the market to consider returning. These changes will improve affordability, but are also likely to generate a degree of pressure on property prices, although this increase should remain moderate.

Despite the expected rebound of activity, Royal LePage maintains its year-end forecast for the Greater Montreal Area and Quebec City, with aggregate prices expected to rise by 8.5% and 9.5%, respectively, in the fourth quarter of 2024, compared to the same period in 2023.

For other regional releases, click here.

Royal LePage House Price Survey Chart: rlp.ca/house-prices-Q3-2024

Royal LePage Forecast Chart: rlp.ca/market-forecast-Q3-2024

Royal LePage’s media room contains royalty-free assets, such as images and b-roll, that are free for media use.

About the Royal LePage House Price Survey

The Royal LePage House Price Survey provides information on the most common types of housing, nationally and in 64 of the nation’s largest real estate markets. Housing values in the Royal LePage House Price Survey are based on the Royal LePage Canadian Real Estate Market Composite, produced quarterly through the use of company data in addition to data and analytics from its sister company, RPS Real Property Solutions, the trusted source for residential real estate intelligence and analytics in Canada. Additionally, commentary on housing market trends and data on price and forecast values are provided by Royal LePage residential real estate experts, based on their opinions and market knowledge.

About Royal LePage

Serving Canadians since 1913, Royal LePage is the country’s leading provider of services to real estate brokerages, with a network of approximately 20,000 real estate professionals in over 670 locations nationwide. Royal LePage is the only Canadian real estate company to have its own charitable foundation, the Royal LePage® Shelter Foundation™, which has been dedicated to supporting women’s shelters and domestic violence prevention programs for 25 years. Royal LePage is a Bridgemarq Real Estate Services® Inc. company, a TSX-listed corporation trading under the symbol TSX:BRE. For more information, please visit www.royallepage.ca.

Royal LePage® is a registered trademark of Royal Bank of Canada and is used under licence by Bridgemarq Real Estate Services® Inc.

Media contact:

Jillianne Gignac

Hill & Knowlton for Royal LePage

jillianne.gignac@hillandknowlton.com

514-929-6170

[1] Aggregate prices are calculated using a weighted average of the median values of all housing types collected. Data are provided by RPS Real Property Solutions and include both resale and new build.

[2] Statistics Canada. Table 18-10-0004-13 Consumer Price Index by product group, monthly, percentage change, not seasonally adjusted, Canada, provinces, Whitehorse, Yellowknife and Iqaluit

[3] Canada Mortgage and Housing Corporation (CMHC). Fall 2024 Housing Supply Report, September 26, 2024

[4] Royal LePage. Royal LePage 2024 Next Generation Survey, August 22, 2024.

[5] Conference Board of Canada, Canadian Consumers are Regaining Confidence, September 25, 2024